Canada’s Most Flexible Benefits Platform

Design your own benefits plan, add your team in minutes, and manage it all in one place. Flexible coverage, built around your business.

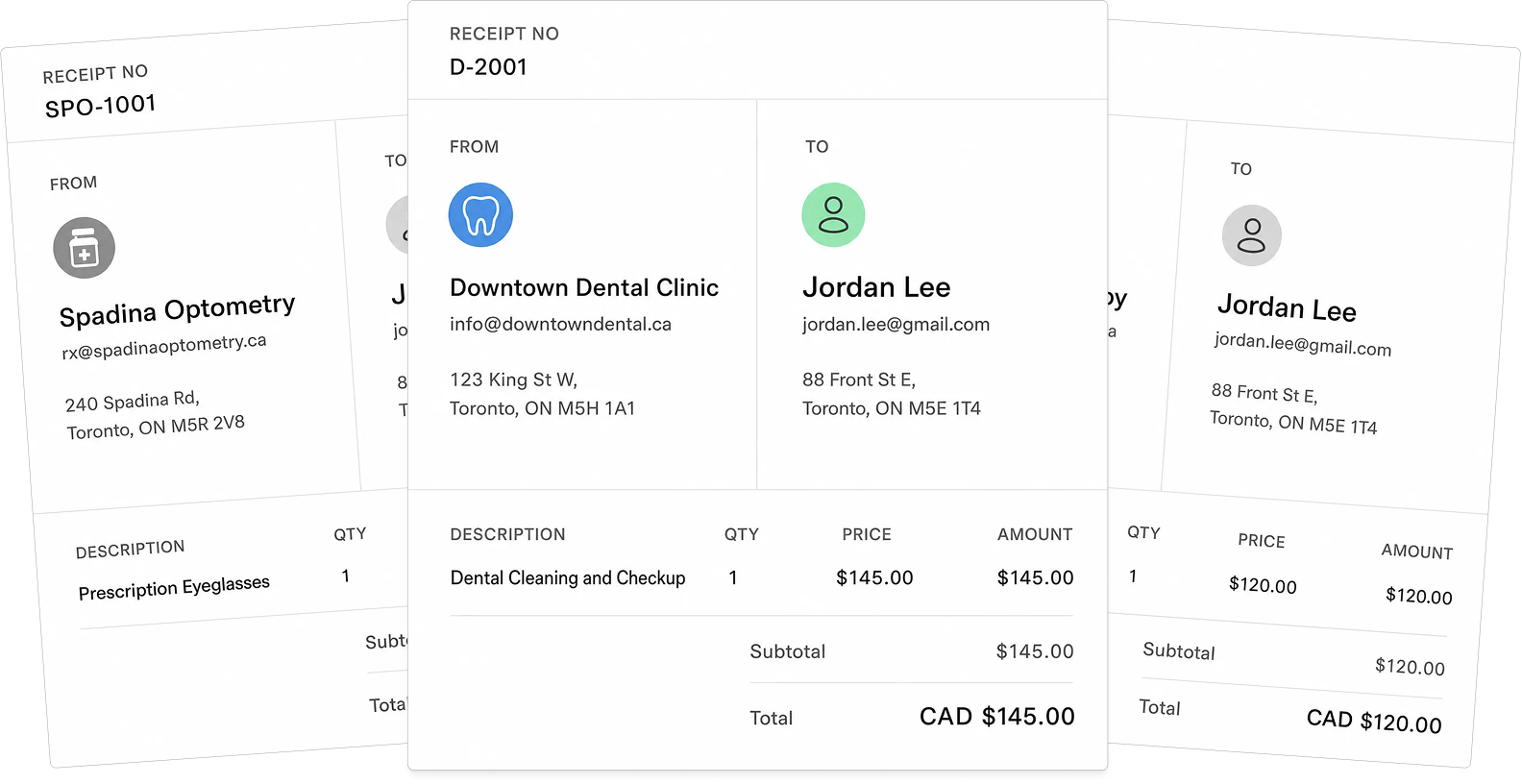

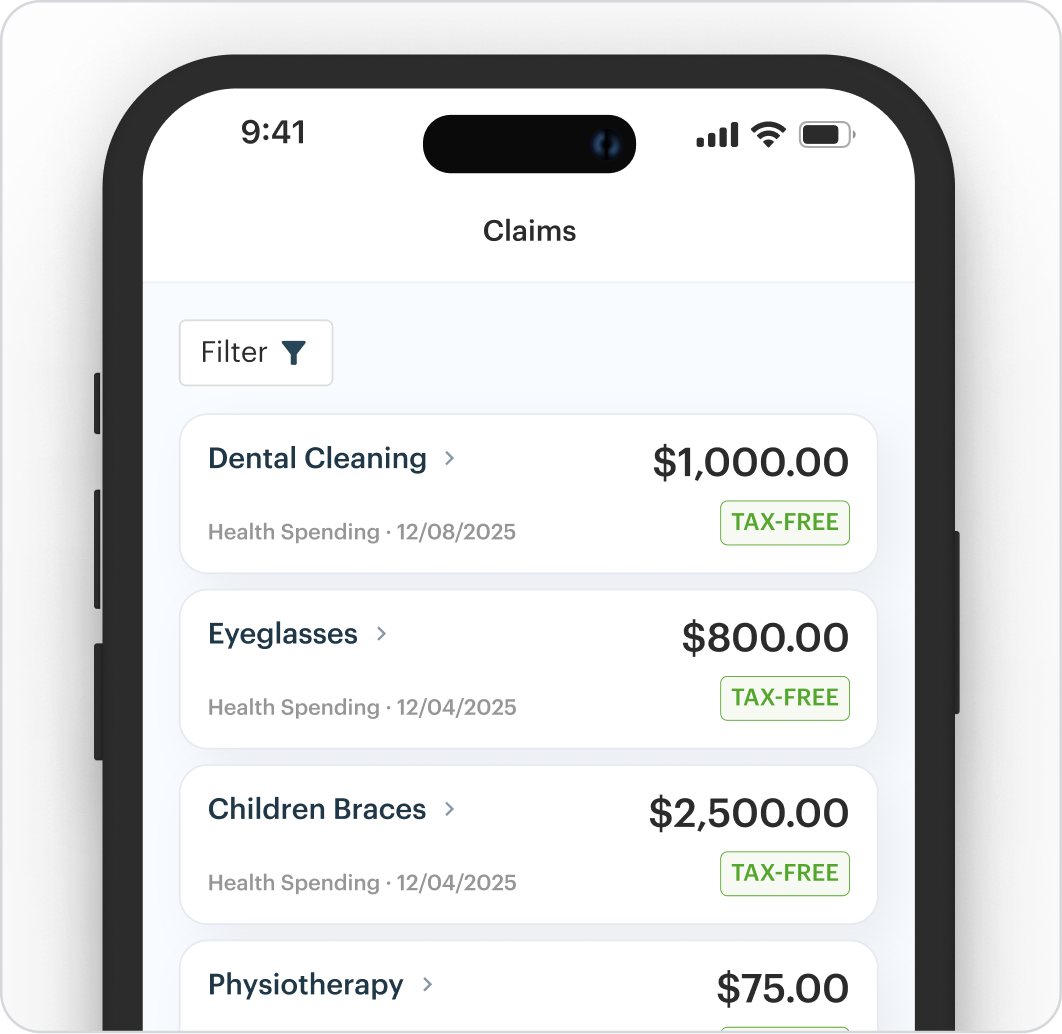

Health (and tax) benefits for incorporated individuals

Finally, coverage for business owners without minimum employee requirements. Claim all your personal and family expenses through your corporation. 100% tax free to you and 100% tax deductible for your business.

Get coverage on your personal and family health expenses

Whether you need to pay for new eyeglasses, braces for your children, or massages for your spouse, our Health Spending Account has got you covered.

100% tax deductible for your business – 100% tax-free to you

Claim all your expenses through your corporation. No more paying out of pocket for your medical expenses.

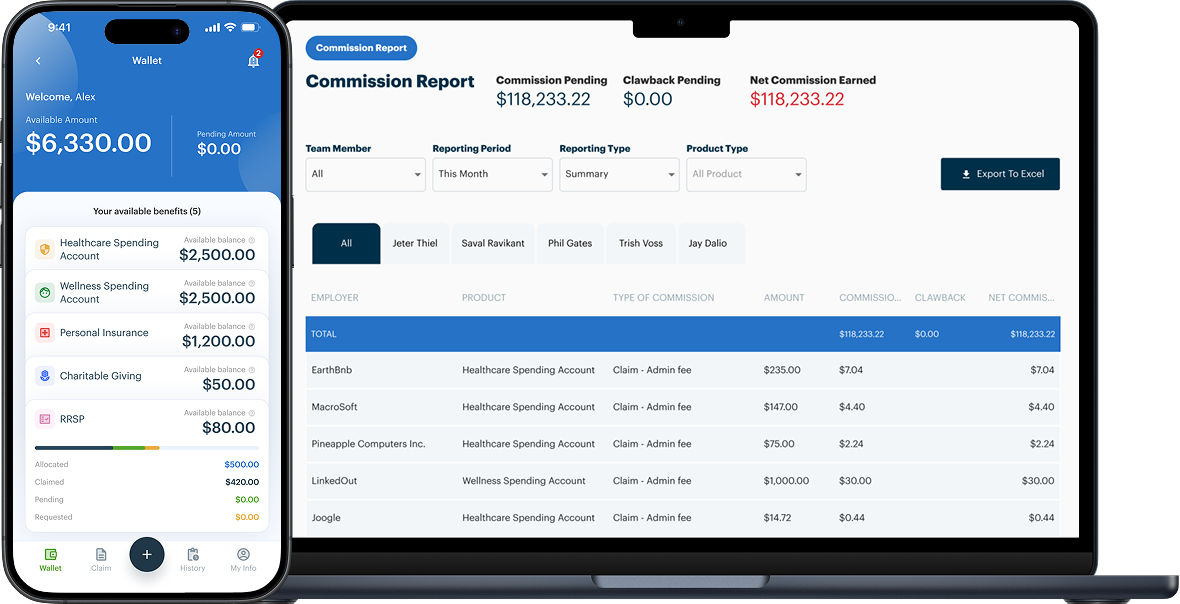

Flexible benefits for companies of all sizes

Flexible employee benefits for your employees and executives. Simple, affordable, and flexible to your needs. No monthly premiums. No contract. Complete cost control.

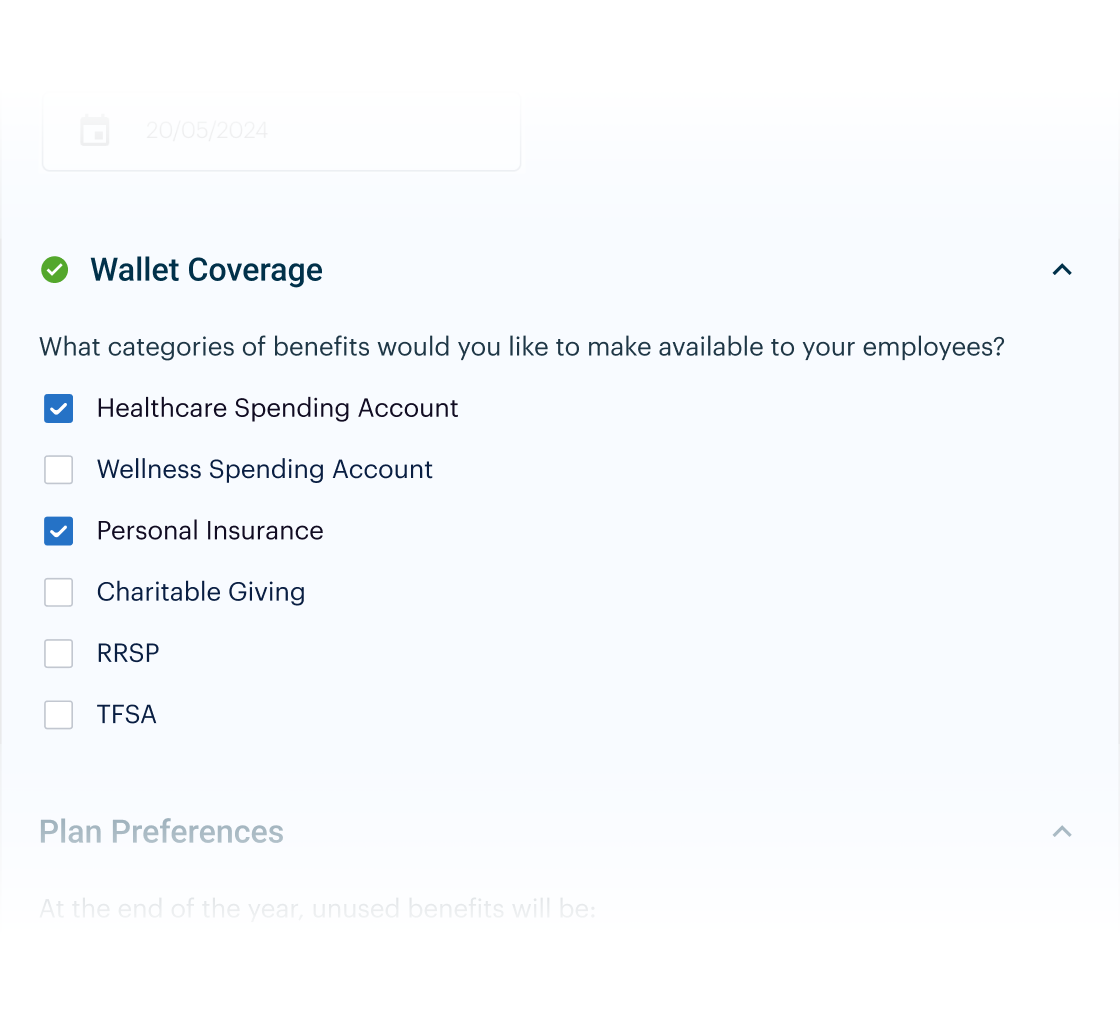

Personalize your plan with up to six benefit categories

Your employees’ needs are unique, and so should your benefits plan. Pick and choose the benefits that matters most to your team, caring for their physical, mental, and financial health.

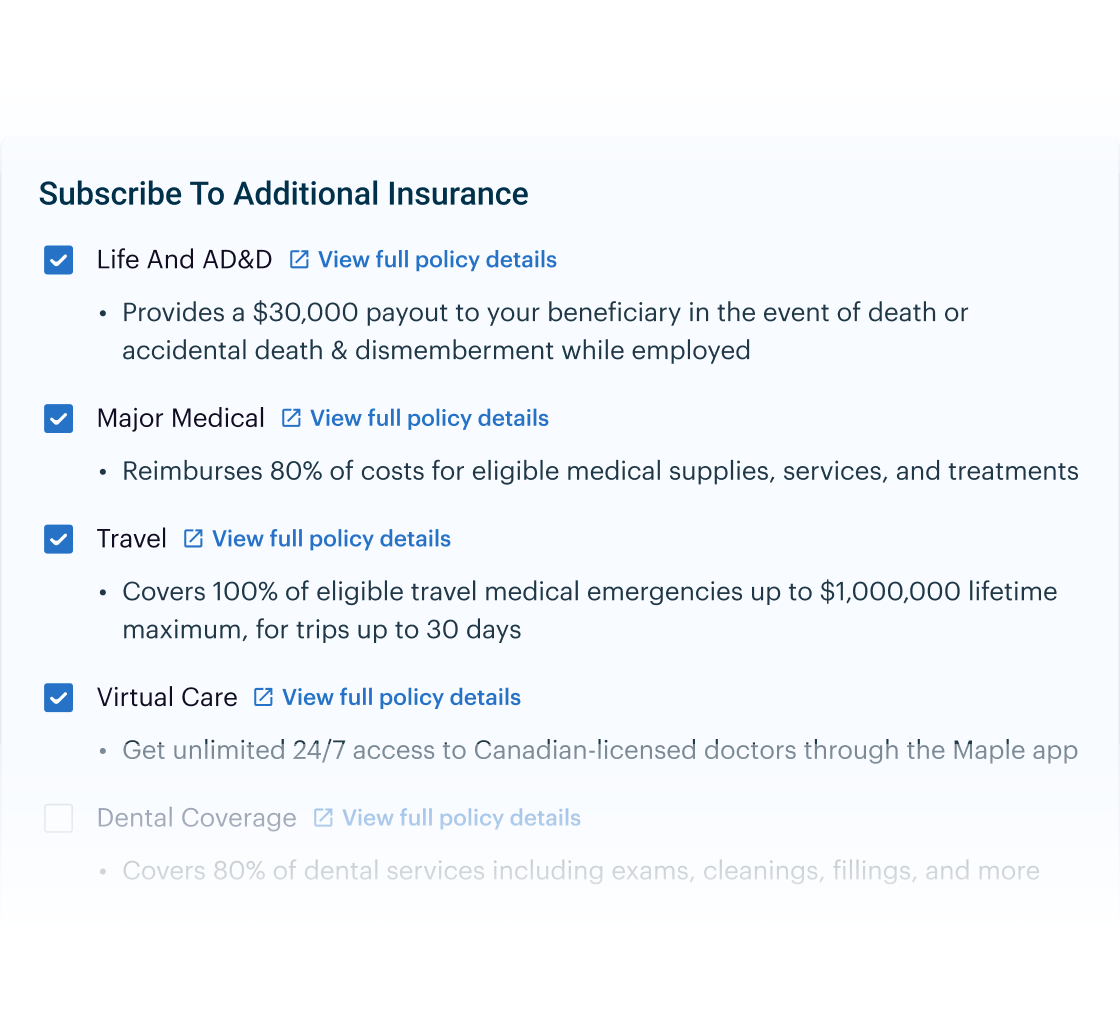

Power up your plan with additional insurance and executive benefits

Claim all your expenses through your corporation. No more paying out of pocket for your medical expenses.

“BeniPlus has allowed our employees to choose to allocate benefits in the areas they actually use depending on their health, wellness, and retirement needs.”

Frequently asked questions

No. There's no medical underwriting on the HSA or our pooled lines, so there are no health questionnaires, no exams, and no one can be rated or declined. Everyone in a class gets the same benefit.

The HSA is built for everyday, predictable costs like dental, vision, paramedicals, and maintenance drugs. For the rare and catastrophic, we pair it with Major Medical: a $2,500 deductible and up to $250,000 of coverage, so you're protected for both the routine and the unexpected.

Yes. Reimbursements are a 100% tax-deductible business expense for you and arrive 100% tax-free for your employee. Because the money never runs through payroll as taxable income, the same medical spending costs about 30% less than paying out of pocket, and it stays fully CRA-compliant.

Traditional plans are claims-driven, so costs swing at every renewal and tend to compound year over year. BeniPlus turns your benefits into a fixed, predictable budget you control, with pooled protection for the catastrophic. Predictable costs, real coverage.

One life. A group of one is fully eligible, including the pooled insurance lines that most carriers won't quote for small teams.

No, it's pay-as-you-go. You only fund what's actually claimed, plus a 10% admin fee and applicable tax. Unused amounts stay with you and never convert into employee compensation.

Get started today

Set up flexible benefits that won’t blow up at renewal. Get a personalized quote in minutes, with no medical underwriting.